The 85/15 Reality: Understanding What KESD Can and Cannot Control in the Budget

March 31, 2026

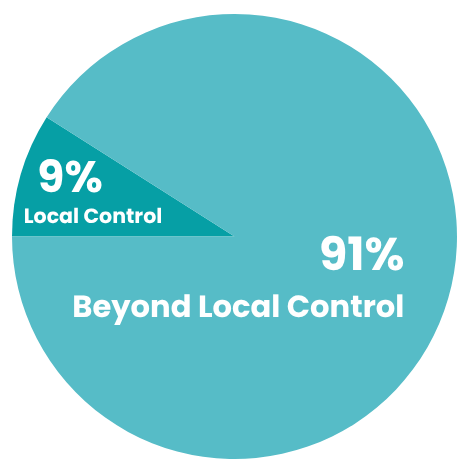

When we talk about school budgets, it is easy to assume that local districts have full authority over how money is spent. The reality is very different. In fact, 91% of KESD’s budget is beyond local control. That means only about 9% of spending decisions can be adjusted at the district level.

This “85/15 rule” (or in this case, an even more extreme version), highlights a critical truth: the vast majority of KESD’s financial obligations are driven by external mandates, statewide agreements, and factors outside the district’s direct influence.

Let’s take a closer look at what makes up that 91%.

High School Tuition

One of the largest pressures comes from high school tuition costs. As more 9th grade students enroll in out of district placements and fewer graduate within four years, tuition expenses rise. These costs are not discretionary. They are tied to student enrollment patterns and contractual obligations with receiving schools.

Healthcare VEHI

Healthcare is another major cost center that KESD cannot directly control. A 7.40% increase in FY27 was determined by statewide bargaining, not local decision making. Over time, healthcare costs have risen dramatically, with a 63.20% increase from FY22 to FY27. Approximately 80% of health plan costs are paid by KESD, but the rates themselves are set externally.

This means the district must absorb rising healthcare expenses without the ability to negotiate independently.

Special Education

Federal mandates require districts to provide appropriate services for all students, including those with specialized needs. KESD currently supports 18 alternative placements, each costing between $100,000 and $150,000 per student, plus transportation.

These services are essential and legally required, leaving little to no flexibility in how funds are allocated.

Contractual Wages and Salaries

Employee compensation is another fixed cost. A 4.60% increase to base wages was implemented through a ratified agreement.

Because these increases are contractually obligated, they cannot be adjusted without renegotiating agreements, which is a complex and infrequent process.

Other Benefits

Beyond salaries and healthcare, KESD must also fund a range of required benefits, including dental and long term disability, worker’s compensation, unemployment insurance, childcare tax contributions, municipal retirement obligations, and teacher OPEB.

These are standardized costs tied to employment and regulation, not local preference.

Why This Matters

Understanding that 91% of KESD’s budget is not in local control reframes how we think about school finance decisions. When budget challenges arise, they are often driven by external cost increases rather than local spending choices. This leaves district leaders working within a very narrow margin, just 9%, to make adjustments, prioritize programs, and respond to community needs.

KESD’s financial picture is not about unchecked local spending. It is about navigating a system where most costs are predetermined. Recognizing this helps build a clearer, more informed conversation about school funding, budget constraints, and the difficult decisions districts must make.

It is also important to understand what this budget represents. KESD is not buying new programs or expanding services. This budget reflects the cost of keeping schools open at current service levels, even after making 25 staffing reductions. The district already operates with lower per pupil spending than the Vermont state average, while continuing to see encouraging growth in student data and outcomes. For taxpayers, income sensitivity tax relief remains available, which can significantly reduce the actual tax impact based on household income.

Sharing Options:

More District News